This article was adapted from a standing-room only presentation given by Mel Larson, Principal Consultant of KBC, a Yokogawa Company, the keynote speaker at RefComm® Galveston 2019.

The abundance in liquefied natural gas (LNG), along with the change in ship bunker fuel sulfur allowance, has put a spotlight on bottom of the crude oil barrel. The world crude oil qualities and demands are constantly changing. Today, sweet crude today is far more abundant than it was 10 years ago. That offers a short-term benefit but it’s not yet clear if there will be a long-term gain. The challenges in processing sweet crude are many and include: well life, cost, and compatibility of existing assets, along with the increased pressure to reduce pollution when managing the carbonaceous bottoms.

In addition, there are market shifts which are negatively impacting refineries. Diesel demands in Europe are falling faster than expected. Efficiency demands are increasing and there are investment challenges. Proven Technology vs Emerging Technology is an obstacle to potential investments. ROCE is critical and cash is not readily available.

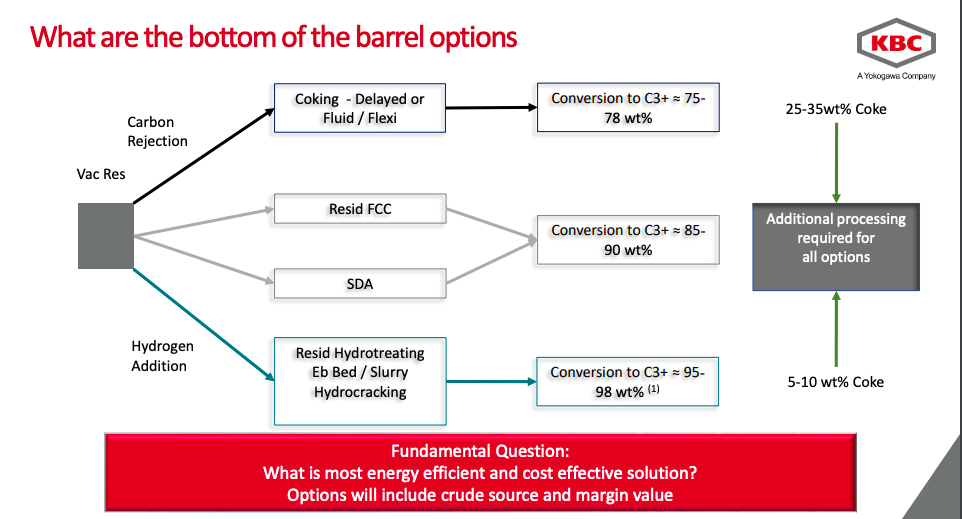

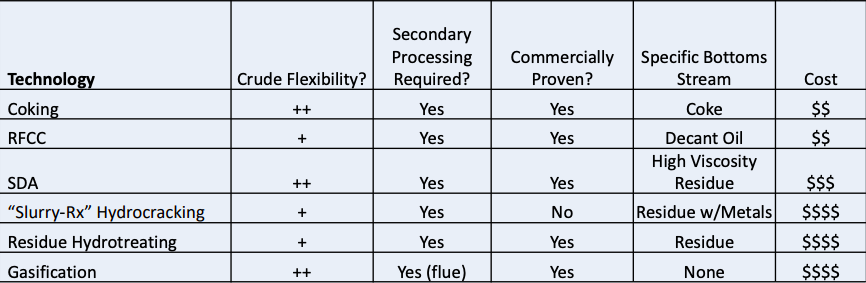

The most often considered pathway for bottoms management has been the carbon rejection route. Delayed coking has been popular for its relative low costs. The delayed coker will provide some with a 70-75% conversion rate. But in light of CO2 reductions, is there a different pathway from carbon rejection to hydrogen addition that is sufficiently mature to be a viable alternative?

There are emerging technologies, such as resid hydrocracking, which adds hydrogen to the bottom of the barrel to maximize the liquid yield for a higher conversion rate and yields more valuable products, ranging from fuels to petrochemical feedstocks, all of which require further processing and additional assets, such as sulfur plants and hydrogen complex systems, not to mention power. The commercial application of these technologies is still limited and yet the overall demand to reduce oil consumption is a driver to maximize the utilization of the molecules and hence reduce the demand of raw crude.

Market Shifts: Past, Present, & Future

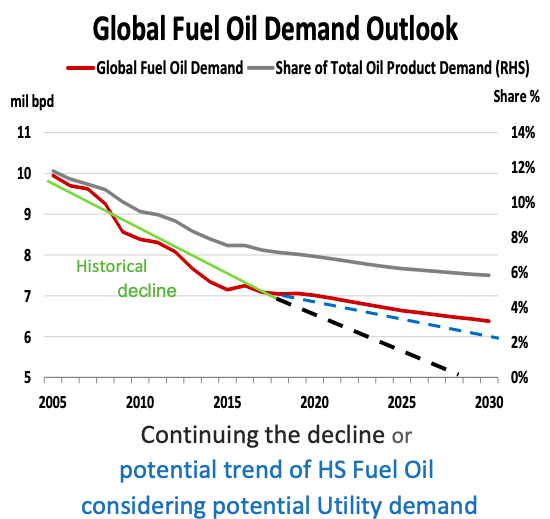

The demand for heavy fuel oil has been in decline since the 1980s, while the demand growth for lighter products (ethane, liquefied petroleum gas, and naphtha) is almost three times greater than that of the total oil demand.

Global residual fuel demand has also been declining for decades, begging the question: what is the future of heavy carbon rich fuel sources?

Chemicals Market

The petrochemicals market continues to grow globally, as do LNG demands, and the U.S. market is expanding with cheap natural gas liquids.

Motor Fuels Demand

The motor fuels industry is flat to declining in the U.S. and Europe, but the market is enjoying a slight increase in South America as well as east of Suez. Fleet efficiencies are on the rise and there is a marked shift in consumer demand.

Back to Front Analysis: Cyclical Demand

With regards to petcoke, the biggest players are China and India. The power generation industry will see a sharp decline, whereas the cement industry can expect a 7% growth through 2025. The steel industry will experience an 8% growth through 2025 and the aluminum industry a 4% growth through 2022. The anode coke growth is fully dependent upon consumer demand and trade issues that are not currently clear.

A general point to remember is that coke as a product– be it fuels or anode quality– contributes less than 5% to the net margin of refinery operations. Therefore, a company must consider forward coke outlets, margin, and ROCE elements in decision making.

The reality is that renewables (biodiesel/ethanol) still emit carbon dioxide. Wind and solar power are inconsistent to a population that demands consistency. Sufficient infrastructure does not and likely will not exist for another 30 years. Motor fuel demand will see regional demand issues with the slope of increase globally lower than historical trends. While at the same time, plastics demands will increase overall, which will be oil-derived sources. Even with increases in recycling, the demand continues.

What does all of this mean to the bottom of the barrel?

Ideally, for every barrel of crude a refinery hopes to generate a barrel of usable product. We have several different process units that provide us with a variety of options when it comes to processing. In a carbon rejection unit like the delayed coker (DCU), there is up to a 75% yield of usable product from the vacuum residue. Resid fluid catalytic cracking (RFCC) and solvent deasphalting (SDA) units provide a slightly better conversion rate. But with the addition of hydrogen, resid hydrocracking yields up to a 95% conversion rate, making it the most efficient with its high conversion rate. But it is also the most expensive method and the technology is still developing and improving, making it a reluctant choice for some refiners.

Shift in Global Refining

We can’t rely on the simple refinery model anymore. As the demand continues for transportation fuels and heating, as well as petrochemicals for use in plastics, we are going to have to do more hydroprocessing. As the quality of the crude decreases, refineries will need to increase their hydroprocessing conversion to maximize efficiency and profitability.

A simple hydroskimming operation in this new future will yield unfavorable economics. The crude diet is limited to sweet options and the Nelson Complexity Index (CI) is at a 5 or less. A cracking refinery complex will fare slightly better, but not by much. It uses a high sulfur Bunker product that will be at greater risk as IMI 2020 comes into effect. These complexes deal in crude diets that are low to medium sour, with a Nelson CI range of 6-9.

A full conversion refinery with a Nelson CI range of 9-12 is better positioned for profit in the future because of its size and flexibility. Its crude diet is limited only by metallurgy and hydroprocessing assets. And a full conversion integrated Petrochemical complex will be insulated from nearly all threats in the future. With a Nelson CI of 13 or greater, it can take on a complete crude diet and turn all byproduct into profit; nothing is wasted.

Capital Investment Risks: Bottoms Conversion

Emergent Choices

Delayed Coker Expansions in the U.S./EU have demonstrated proven technology and they have access to discounted sour crude. East of Suez there are a mix of technologies. In India, there is delayed coking, and slurry hydrocracking is strong in China and Russia. And flexicokers are reemerging. Major factors include cost, reliability of technology, and the disposition of the coke.

Decisions moving forward will be based upon the margin value, and what will drive crude diet in the future will be the sweet-to-sour crude differential. The anticipated IMO impact will likely widen that spread, and those who can process more heavy sour will make profit while those who can only process sweet will be pinched.

There is no simple answer or a silver bullet, but any successful approach moving forward will require that our industry become more efficient. We need to focus on achieving reduced variable costs and energy efficiency. We should consider raw material to finished product and the value chain optimization. And the industry needs to be responsive and adaptive through digitalization and other emerging technologies.

Previously, bottom of the barrel was U.S.-centric and not considered on a global scale. Under a global consideration, we need a more focused discussion on crude quality, region, access to capital, and maturity of market — these will be the major players in successful decisions moving forward.

Click here to access Mel Larson’s full presentation.

For other past RefComm® presentations, visit https://refiningcommunity.com/past-presentations/.

Click here to learn more about RefComm® Rotterdam 2019 and here for Mumbai 2019.

For more information about KBC, visit the company’s website.

One response to “Bottom of the Barrel Conversions: What Does the Future Hold?”

Leave a Reply

[…] Bottom of the Barrel Conversions: What Does the Future Hold? […]